If you run or are starting an online business selling to customers in Europe, you’ve heard about value-added tax (VAT).

Like any other tax, VAT isn’t an exciting dinner table conversation topic. But you need to understand it to run a profitable online store (and avoid trouble with the tax office).

Get up to speed on e-commerce VAT rules with our digestible primer.

When e-commerce companies need to collect VAT?

If your company is registered in the EU and/or sells to local customers, you’ll need to apply and remit value-added tax.

VAT applies to:

- B2C sales — all deal-making with EU private individuals.

- Imported goods — supplies brought from outside the EU to trade locally, charged at the border upon entry.

- Digital products and services to consumers or businesses without a VAT number are subject to VAT in their country of residence.

- B2B sales, but with a caveat. VAT applies to domestic B2B sales (e.g., from an Estonian office goods supplier to a local business). But no VAT is due to cross-border B2B transactions (e.g., between an Estonian and Spanish business) thanks to the Reverse Charge Mechanism.

When don’t I need to collect VAT?

There are several cases when you don’t have to worry about your VAT obligations:

- Sales to non-EU customers. Goods exported outside the block — to the US, Canada, Peru, or Tuvalu — aren’t subject to EU VAT. But other local sales taxes may apply.

- Low domestic turnover. If you run a hobby resale business as a sole proprietor and bill beyond the VAT threshold in your country, you don’t need to collect VAT. Each country has a different VAT threshold for small businesses.

- Small cross-border footprint. Starting January 2025, e-commerce operators can register as SME VAT-exempt (less taxes and easier compliance) if their annual turnover is below €100,000 total and they don’t exceed local thresholds in any of the EU countries.

In all other cases, you must collect and remit VAT on e-commerce transactions. This can be tricky because each EU member state has different VAT rates and remittance rules.

What VAT Rates Do I Charge on E-Commerce Sales?

The VAT rate will depend on the shipping destination and dispatch point:

- Domestic market sales. If you’re selling to your compatriots (e.g., a Spanish biz, shipping espadrilles locally), charge and remit a Spanish VAT rate of 21%. That’s simple. And a Spanish VAT number will be required.

- Cross-border EU sales. If you sell to consumers in other countries (e.g., an Estonian store shipping woolen sweaters to Finland), apply the buyer’s country’s VAT rate (e.g., 25.5 %). In the case of B2B sales to a foreign buyer with a valid VAT number, you can apply a 0% VAT rate.

Since 2021, Europe has a single-distance selling threshold of €10K per year. If your total sales to all other EU countries are below €10K, you can use your home country’s VAT rate. If sales exceed ten grand, you’ll need to apply variable VAT rates for each country.

Here’s a quick example to illustrate this rule:

Last year, you sold €8,000 worth of goods to consumers in Poland, Germany, and Italy. For these sales, you can charge a local VAT rate (e.g., 22% if you have a registered company in Estonia) with your local VAT number.

But since the start of this year, you’ve already sold €9,500 worth of goods to the same countries. This means you need to register for the One-Stop-Shop (OSS) scheme (more on this in the next section!) and start applying customers’ domestic rates in each country (e.g., 23% for Polish buyers, 19% for Germans, and 22% for Italians).

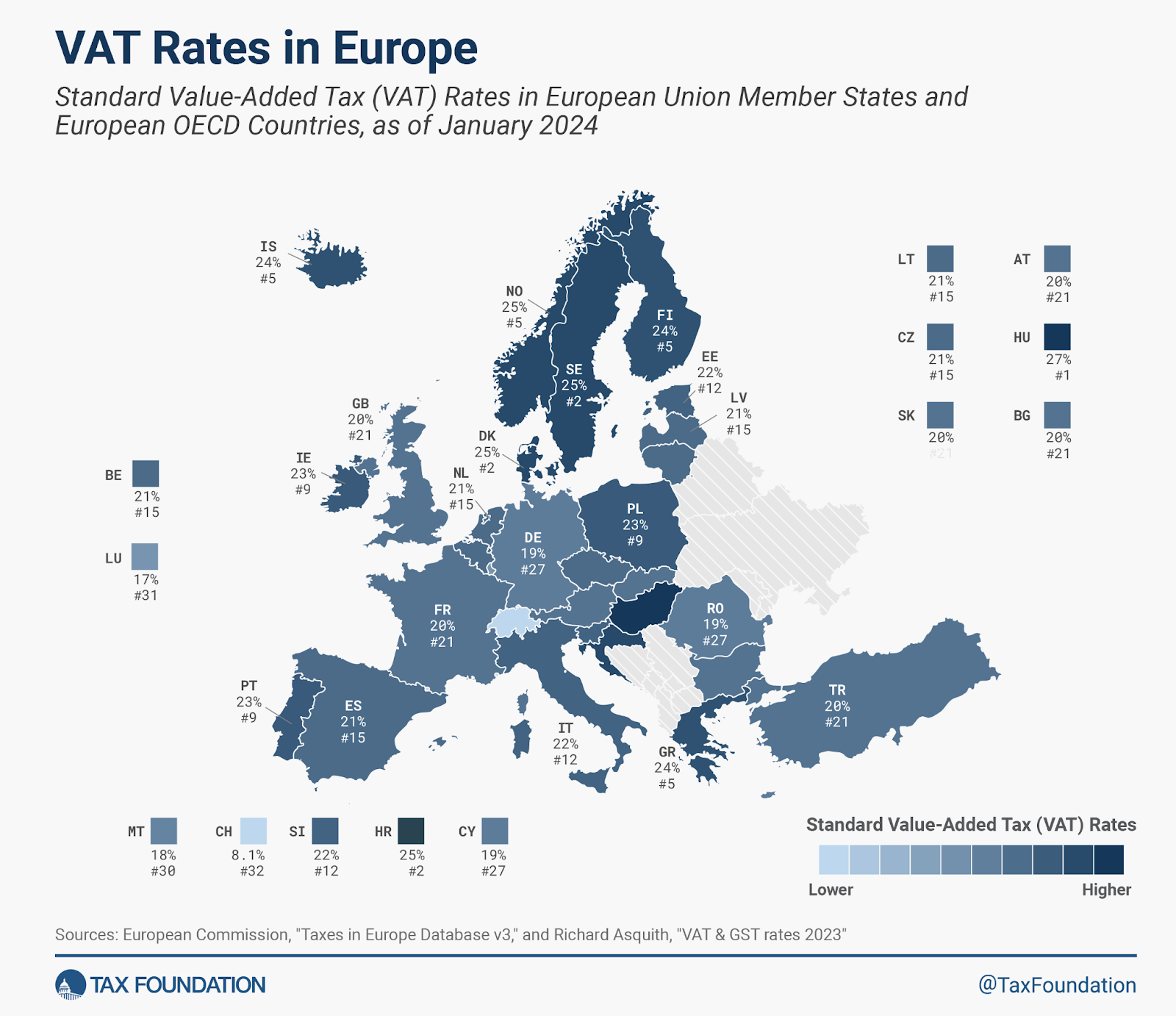

VAT rates in the EU

Source: Tax Foundation

The good news is you don’t have to register as a taxpayer in every state where you sell, thanks to the One-Stop-Shop (OSS) system.

One-Stop Shop (OSS) and Import One-Stop Shop (IOSS) explained

To simplify VAT compliance for EU online sellers (and everyone else doing business in the market), the authorities created two handy schemes: OSS and IOSS.

VAT OSS

The one-stop-shop scheme (OSS) concerns VAT payments across EU markets. Its goal — simplify VAT application and remittance for e-commerce companies operating in different countries.

OSS allows e-com operations to file one consolidated VAT report for all B2B sales, instead of juggling submissions to dozens of different tax offices.

Register for OSS once your cross-border EU sales exceed €10,000 per year.

Each EU country has its own OSS registration portal, usually on its national tax authority’s website. In Estonia, it’s Maksu- ja Tolliamet (Tax and Customs Board), with whom you can interact digitally (and in English!) if you run an e-Residency company.

To register for VAT OSS, you’ll need to have a valid VAT number and then complete an online form with the following details:

- Business name and address

- Contact details (email, phone number)

- Valid VAT number

- Bank account details

- Information about your business activities

Once done, you’re set to report and pay VAT on cross-border sales.

Onward, here’s how things will work:

- Charge local VAT rates for each customer (e.g., 20% in France and Belgium, 25% in Sweden). Always include the correct VAT rate on your e-commerce invoice next to the product price.

- Submit a single VAT return quarterly via the OSS portal. Your local tax office will then determine your VAT obligations in each country.

- Pay one tax bill. Settle the grand total once and the tax office will route all VAT payments to respective countries.

Without VAT OSS, you’d need to register for VAT in each country where you make sales and deal with each country’s tax office independently (hardly exciting). OSS simplifies this to one report and one payment, saving you a massive hassle.

For even simpler e-commerce VAT reporting, get help from Xolo. We provide an invoicing tool, integrated banking services, payment processing, and e-commerce accounting support, covering OSS registration and all tax form submissions to the Estonian Tax and Customs Board.

VAT IOSS

Import one-stop-shop (IOSS) scheme is a similar system for reporting import VAT — payment is due once the sale is made and the goods are sent to a consumer in the EU member state from outside the block.

For instance—you import US-manufactured goods or dropship products from China. Or you're incorporated in a non-EU market (e.g., New Zealand) and sell goods in several European markets.

The IOSS scheme streamlines VAT reporting for all European B2C sales below €150 per order.

Here’s how IOSS works in practice. Let’s say you’re selling handmade jewelry from Indonesia in Europe. An Estonian customer buys earrings for €30. The Estonian VAT rate is 22%, so you charge €36.60 at checkout (€30 + €6.60).

When shipping the product, include your IOSS number at customs. When it crosses the border, the customer won’t pay VAT (only applicable customs charges for orders above €150). You’ll report the VAT transaction via the IOSS system and pay all dues in one lump sum.

According to the Baymard Institute, high extra costs like shipping, taxes, and handling fees are the #1 reason for cart abandonment. Even if people check out, they may refuse to pay import taxes (which happens often), leaving your order in customs limbo.

IOSS helps avoid such scenarios. During checkout, shoppers can see the final price and decide if they’re buying from you. Since all taxes are pre-paid, your shipment also clears customs faster, making customers happier.

To register for VAT IOSS, you’ll need to:

- Log in to your country’s tax authority website and find the registration page.

- Provide your business name, tax number, and type of goods you sell.

- Get your IOSS VAT number for customs declarations for all shipments from outside the EU.

Once you’re set, charge the buyer’s VAT rate, submit monthly IOSS VAT returns, and pay the total bill. Once again, Xolo e-commerce accounting team would be happy to help with IOSS registration and ongoing compliance.

What if I import products, valued at over €150 a pop?

In this case, you’re not eligible for the IOSS scheme. Instead, VAT and customs duties will be collected at the point of import (i.e., the city/country, where your products enter the EU) by the local customs office.

You have two delivery options then:

- Offer Delivery Duty Paid (DDP) — pre-pay VAT and other applicable duties for the customer, often via your logistics partner.

- Offer Delivery Duty Unpaid (DDU) — leave VAT and duty payments to the customer.

When filling out a customs declaration, you’ll need to state who will be the Importer of Record (IOR) — the side responsible for tax payments.

How to manage e-commerce VAT like a pro

To make VAT collection less of a hassle, follow the next e-commerce accounting best practices:

Remember all the Important Tax Thresholds

Remember: VAT obligations kick in at different stages of your business growth.

Suppose you’re just starting in your domestic market only. In that case, you can delay VAT registration until either:

- You’re purchasing under €10K of goods during a taxable year and don’t buy any digital services from outside the country of registration

- Your e-commerce business hits the local VAT threshold (e.g., €40,000 in Estonia, €65,000 in Italy, etc).

Or you can register for SME VAT exemption starting this year if you expect a turnover below €100,000 in total.

The above, however, only applies if you’re sourcing or producing goods within the EU. If your wares come from elsewhere, you’ll need to register for the IOSS scheme and collect VAT on orders below €150.

Create a VAT taxonomy for all sold goods

VAT compliance is challenging because of rate variability. Each EU country has a different standard rate, plus some also allow reduced or zero VAT rates for certain product categories.

For example, Estonia has a reduced VAT rate of 9% for most books and educational literature, medical products, and press publications. The Netherlands also offers a 9% rate for most food, drink, and agro products, plus some artwork, collectibles, and antiques, along with books, press publications, and medicine.

Create a quick reference table, featuring all applicable VAT rates in markets, where you operate. Your e-commerce platform, accounting app, or logistics partner may also offer pre-programmed rates for most markets.

Keep an Eye on the Changes

Governments also decide to change VAT rates relatively often. Last year:

- The Estonian standard VAT rate went to 22% from 20%, and there’s a potential VAT increase to 24% in 2025.

- Luxembourg increased the standard VAT rate from 16% to 17%, reduced rate — from 7% to 8%, and the intermediate rate — from 13% to 14%.

- Finland increased its standard VAT rate from 24% to 25.5%, from September 2024.

The EU regulators are also discussing a wider overhaul of the block’s VAT system to further homogenize rules for online selling among member countries. Nicknamed VAT in the Digital Age (ViDA), the new proposal finally got a unanimous “in favor” vote in November 2024.

As part of ViDA, the EU regulators plan to:

- Make e-invoices mandatory for all domestic sales in the first half of 2025. And then progressively introduce e-invoicing for other types of transactions including cross-border business-to-business (B2B) and business-to-government (B2G) supplies. Some of the invoice data will also have to be digitally reported to the tax authorities.

- Establish a new Single VAT Registration (SVR) scheme from July 1, 2028. It will expand the OSS regime to include more B2C suppliers including electricity, natural gas companies, supply-and-install contracts, and intra-EU movements of own goods. The reverse-charge mechanism will become mandatory for non-established B2B suppliers, reducing VAT registration requirements.

- VAT charges for live events and virtual shows. From 1st January 2025, hosts of live virtual events will have to collect the domestic VAT of the participants. In other words, if your viewers come from France, Germany, and Sweden, you’ll have to charge different VAT rates for each of them and remit VAT via OSS. And if the participants are B2B customers from another EU state, you can avoid VAT thanks to the reverse charge mechanism.

Other changes to VAT rules may also emerge in between, so it always helps to have an experienced compliance team. Xolo always keeps our customers in the loop about upcoming changes to tax rates, reporting requirements, and other areas of regulatory compliance.

Discover how we make e-commerce accounting simpler for Estonia-registered companies!